My Messy Journey with ETFs vs Mutual Funds

ETFs vs mutual funds—man, I’ve been down this rabbit hole, and it’s messier than my desk right now, which is saying something since I just knocked over my coffee trying to type this. I’m sitting in my cramped apartment in Chicago, the radiator hissing like it’s judging me, and I’m thinking back to when I first tried to “get serious” about investing. I was 27, had a couple grand from a freelance gig, and thought I’d be the next Warren Buffett. Spoiler: I’m not. But I learned a ton about ETFs and mutual funds, mostly by screwing up, and I’m gonna spill it all—warts and all.

Back then, I was that guy who thought mutual funds were the “safe” choice because, like, my dad’s financial advisor swore by them. I dumped my cash into one, feeling all adult, only to realize later the fees were eating my returns like termites. ETFs? I didn’t even know what they were until I stumbled across a Reddit thread while procrastinating at a coffee shop in Wicker Park. That’s when I started comparing ETFs vs mutual funds, and let me tell you, it felt like choosing between a kale smoothie and a burger—both can work, but they’re wildly different vibes.

What Are ETFs and Mutual Funds, Anyway?

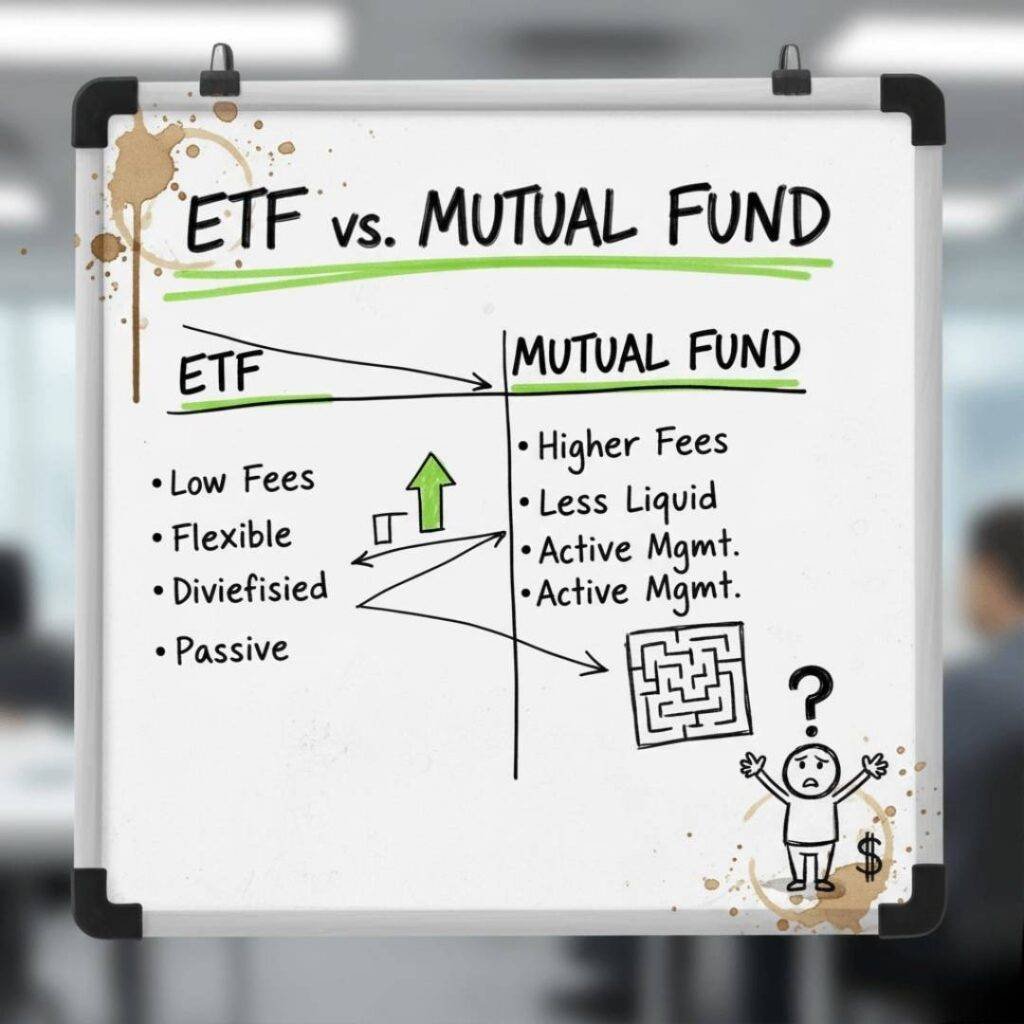

Okay, let’s break this down like I’m explaining it to my buddy over beers. ETFs—exchange-traded funds—are like these baskets of stocks, bonds, or whatever, that trade on the stock market like a single stock. You can buy or sell them all day, and they’re usually dirt-cheap because they’re often passively managed, tracking some index like the S&P 500. Mutual funds? They’re also baskets of investments, but they’re actively managed by some suit who’s supposedly a genius, and you can only buy or sell at the end of the day. Oh, and they often come with fees that make you wanna cry.

- ETFs: Low fees (think 0.03-0.5%), flexible trading, tax-efficient. Great for control freaks like me who check their portfolio too often.

- Mutual Funds: Higher fees (0.5-2% or more), less flexibility, often actively managed. Good if you trust someone else to do the heavy lifting.

I learned this the hard way when I saw my mutual fund’s expense ratio—1.2%!—and realized I was basically paying for some fund manager’s yacht. Meanwhile, my buddy who’s all about low-cost ETFs was flexing his Vanguard ETF with a 0.04% fee. Brutal.

Why ETFs Feel Like My Jam

Here’s where I get real. ETFs vs mutual funds? I lean hard into ETFs now, but not without some dumb mistakes. A couple years ago, I was in a Starbucks in the Loop, scrolling through my Robinhood app (don’t judge, I was young), and I bought an ETF because it had a cool ticker symbol—SPY. Yeah, I didn’t even know it tracked the S&P 500. I just liked the name. But then I saw how cheap it was to hold, and I could trade it whenever I wanted, which was great for my anxious, check-the-market-every-hour self.

ETFs are awesome for people like me who want low-cost investing and don’t trust some fund manager to make better picks than a monkey throwing darts. According to Investopedia, ETFs have lower expense ratios on average—0.44% vs 0.93% for mutual funds. That’s real money when you’re investing for years. Plus, ETFs are tax-efficient because they don’t churn stocks as much, so you’re not hit with surprise capital gains taxes. I learned that one after a nasty tax bill in 2023. Oof.

But Mutual Funds Aren’t Total Trash

Okay, I’m not gonna lie—mutual funds have their moments. I got suckered into one because the advisor promised “active management” would beat the market. Spoiler: it didn’t. But for some folks, especially if you’re not into micromanaging your portfolio, mutual funds can be set-it-and-forget-it. They’re good for retirement accounts where you don’t need to trade daily. My mom’s got a mutual fund in her 401(k), and she’s happy not thinking about it. According to Morningstar, actively managed mutual funds can outperform in niche markets, like small-cap stocks, but only about 20% beat their benchmarks long-term. Yikes.

Still, I tried a mutual fund again last year, thinking I’d learned my lesson. I picked one focused on tech stocks, and it felt like betting on a horse race—exciting but stressful. The fees killed me, and I bailed after six months. Maybe I’m just not a mutual fund guy.

My Biggest Investing Fumble (and What I Learned)

Here’s a cringe story. In 2022, I was at a dive bar in Logan Square, hyped up on cheap IPA, and decided to YOLO $1,000 into a mutual fund because the bartender mentioned it. Yeah, I know. The fund tanked 15% in three months, and I was out $150 in fees alone. That’s when I swore off high-fee funds and started digging into low-cost ETFs. I found Vanguard’s site super helpful for understanding ETF options, and I switched to a broad-market ETF that’s been way kinder to my wallet.

Lessons? First, don’t invest based on bar chats. Second, always check the expense ratio—ETFs usually win here. Third, ETFs vs mutual funds isn’t just about fees; it’s about how much control you want. ETFs give me flexibility, but mutual funds might work if you’re lazier than me (no shade).

ETFs vs Mutual Funds: My Hot Take on What’s Smarter

If I’m being honest, ETFs vs mutual funds depends on your vibe. ETFs are my go-to because I’m cheap and like control. They’re great for passive investing, low fees, and not getting slammed with taxes. Mutual funds? They’re fine if you want someone else to drive, but you’re paying for the ride. I’d rather spend that money on coffee or, like, actual stocks.

Here’s my advice, straight from my fumbles:

- Start small: Try a low-cost ETF like VTI or SPY to dip your toes.

- Check fees: Anything over 0.5% is a red flag unless it’s a niche fund.

- Know yourself: If you’re lazy, mutual funds might be your jam. If you’re obsessive like me, ETFs are where it’s at.

Wrapping Up This Investment Rant

So, ETFs vs mutual funds? I’m team ETF, but I get why mutual funds work for some. I’m just a guy in Chicago, surrounded by empty LaCroix cans and a laptop full of stock charts, trying to make sense of my money. If you’re picking, think about fees, control, and how much you wanna babysit your investments. Got thoughts? Hit me up in the comments or on X—I’m @SomeInvestorDude (not really, but you get it). Seriously, let’s talk investing over virtual beers.

{kind=link}