My Credit Score Mortgage Rate Fiasco: Where It All Started

Man, your credit score mortgage rate situation can make or break your home-buying dreams, and I learned that the hard way. Sitting in my tiny Seattle apartment, surrounded by the smell of burnt toast (yep, I ruined breakfast again), I was staring at my laptop, trying to figure out why my mortgage rate quotes were all over the place. Like, seriously, one lender was offering me 3.5%, and another was hitting me with a soul-crushing 5.2%. What gives? Turns out, my credit score—let’s just say it wasn’t exactly screaming “responsible adult.” I’m talking a 650, which, in mortgage land, is like showing up to a job interview in flip-flops.

Back in 2023, I was clueless about how much your credit score impacts your mortgage rate. I thought, “Eh, I pay my bills… mostly.” But when I saw those interest rates, my stomach dropped like I’d just missed the last bus home. I dug into it, and let me tell you, the connection between your credit score and your mortgage rate is tighter than my budget after a Starbucks run.

Why Your Credit Score Is the Boss of Your Mortgage Rate

Your credit score is like the bouncer at the mortgage club—it decides whether you get the VIP treatment or pay through the nose. Lenders use your score to gauge how risky you are. Higher score? You’re the golden child, getting lower mortgage interest rates. Lower score? You’re stuck with higher rates, and trust me, those extra percentages add up like my laundry pile.

Here’s the deal, straight from my frazzled research:

- Excellent Credit (760+): You’re looking at the best mortgage rates, like 3-4% on a 30-year fixed loan (based on 2025 averages from Freddie Mac).

- Good Credit (700-759): Still decent, maybe 4-4.5%. Not bad, but you’re not winning any awards.

- Fair Credit (620-699): Oof, rates climb to 4.5-5.5%, and you’re paying thousands extra over the loan’s life.

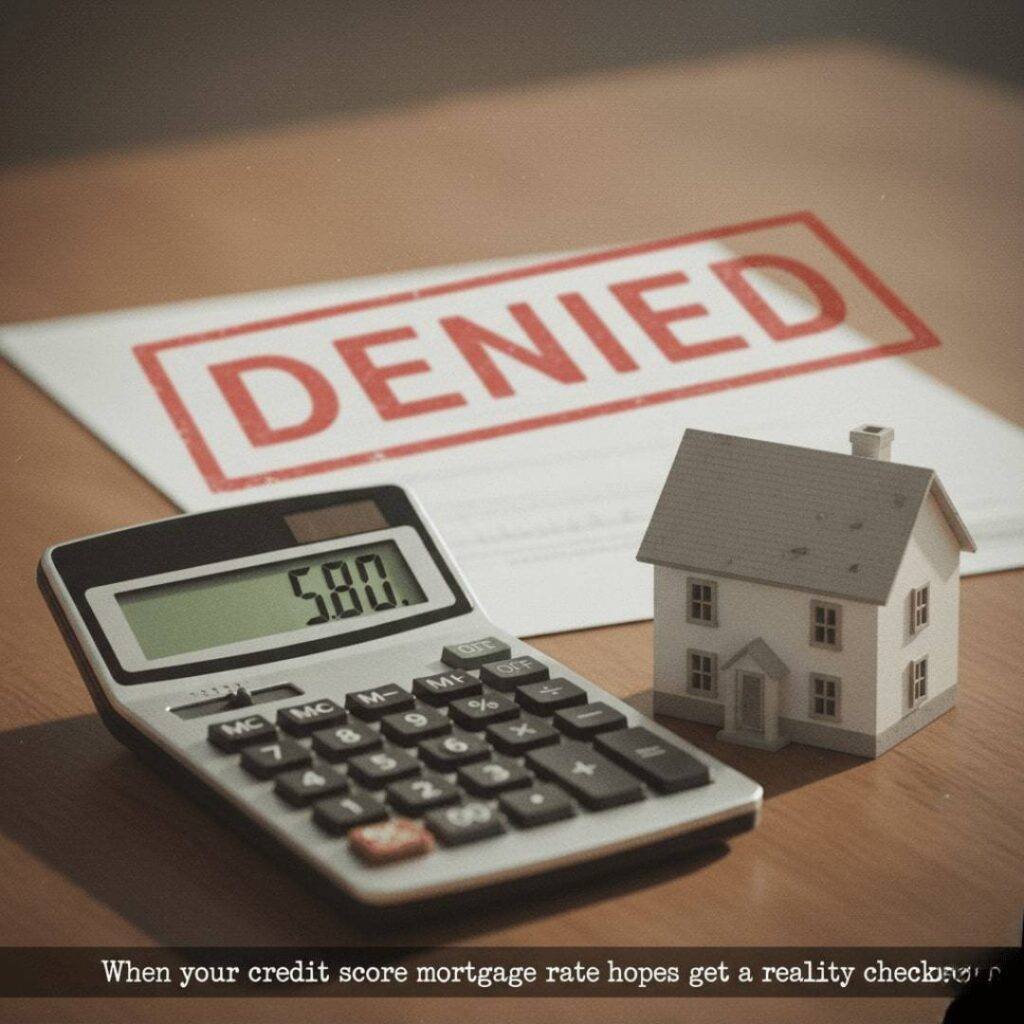

- Poor Credit (<620): Good luck. Rates can hit 6% or more, and some lenders won’t even talk to you.

I was in that “fair” zone, and let me tell you, it stung. I remember pacing my living room, tripping over my cat’s toy, muttering, “Why didn’t I pay off that stupid credit card?” My score wasn’t terrible, but it wasn’t winning me any low-rate love either.

How Credit Score Affects Mortgage Rate Math

Let’s break it down with some numbers, because I’m a nerd like that now. Say you’re borrowing $300,000 for a 30-year fixed mortgage:

- At 3.5% (great credit): Monthly payment is about $1,347. Total interest over 30 years? Around $185,000.

- At 5% (my mediocre credit): Monthly payment jumps to $1,610, and total interest is a whopping $279,000.

That’s almost $100,000 more just because my credit score was meh. I nearly choked on my coffee when I ran those numbers on my calculator, which, by the way, is now my best friend.

My Embarrassing Credit Score Mistakes (Learn from Me, Okay?)

I’m gonna be real—my credit score took a hit because I was, like, tragically bad at adulting a few years back. Picture me in my old Portland apartment, eating instant ramen, ignoring those “past due” emails from my credit card company. I thought, “I’ll deal with it later.” Spoiler: Later never comes, and your credit score pays the price.

Here’s what tanked my score (and how it jacked up my mortgage rate):

- Late Payments: I missed a couple of credit card payments in 2022 because I was “too busy” binge-watching reality TV. Each late payment can drop your score by 50-100 points, according to Experian.

- High Credit Card Balances: I was maxing out my cards like it was a sport. Keeping your balance above 30% of your credit limit? Bad news for your FICO score.

- Ignoring My Score: I didn’t even check my credit until I started house-hunting. By then, it was too late to fix it quickly.

I’m not proud of it, but I’m sharing this because I know I’m not the only one who’s been a hot mess with money. If you’re reading this and nodding, check your score now on sites like Credit Karma or AnnualCreditReport.com. Don’t be me, okay?

Tips to Boost Your Credit Score for a Better Mortgage Rate

I’ve been working on my credit score like it’s my new side hustle, and I’ve picked up some tricks. Here’s what’s helping me claw my way to a better mortgage interest rate:

- Pay on Time, Every Time: Set up auto-payments. I did this after forgetting a bill during a Netflix marathon. No more excuses.

- Lower Your Credit Utilization: Pay down those cards. I threw every extra dollar at my balance, and my score crept up 30 points in a few months.

- Don’t Apply for New Credit: Every application can ding your score. I learned this after impulsively signing up for a store card. Dumb move.

- Check for Errors: My report had a random medical bill I didn’t owe. Disputing it with TransUnion bumped my score a bit.

It’s not overnight, but even a 50-point boost can shave your mortgage rate down and save you thousands.

Multimedia Suggestion: Images to Bring This Credit Score Mortgage Rate Saga to Life

The Emotional Rollercoaster of Credit Scores and Home Loans

Here’s the thing—I’m still kinda mad at myself for not taking my credit score seriously sooner. Every time I walk past a cute house in my neighborhood, I imagine what could’ve been if I’d had a better mortgage rate. But I’m also weirdly hopeful? Like, I’m fixing my score, bit by bit, and maybe next year I’ll be in a better spot. It’s this bittersweet mix of regret and “I got this” energy.

I’m sitting here now, typing this in my cluttered living room, with my cat glaring at me for knocking over her water bowl (sorry, Luna). The rain’s tapping on my window, and I’m thinking about how your credit score isn’t just a number—it’s your ticket to a home, a future, or at least a chance to stop renting. It’s personal, messy, and yeah, sometimes it makes you wanna scream into a pillow.

Wrapping Up: Don’t Let Your Credit Score Mortgage Rate Dreams Crash

So, yeah, your credit score impacts your mortgage rate in a big way, and I’m living proof of what happens when you don’t pay attention. I’m still working on my score, still dreaming of that house, and still occasionally burning my toast. If you take one thing from my chaotic ramble, it’s this: check your credit score today. Fix those little mistakes, pay down those cards, and don’t be like me, stressing in a Seattle apartment over a 5% rate.

{kind=link}