Man, picking between a fixed vs adjustable mortgage is like choosing between a steady job and a gig economy hustle. I’m sitting here in my tiny Ohio apartment, coffee mug leaving rings on a stack of bills, trying to figure out which one’s gonna save me more in the long run. It’s October 2025, the leaves are turning, and I’m still haunted by the time I almost signed an adjustable-rate mortgage (ARM) without reading the fine print. Spoiler: I’m not a financial wizard, and my story’s got some cringeworthy moments. But let’s dive into this fixed vs adjustable mortgage mess, because I’ve been there, and I’m betting you’re stressing about it too.

Why I Even Started Thinking About Fixed vs Adjustable Mortgages

A couple years back, I was house-hunting in Columbus, Ohio, dreaming of a backyard for my dog, Rufus. The realtor kept tossing around terms like “fixed-rate” and “ARM” like I was supposed to nod knowingly. I didn’t. I was too busy picturing Rufus chasing squirrels while I panicked over a spreadsheet. My first mistake? Thinking an adjustable-rate mortgage sounded “flexible” and cool, like yoga for my wallet. Turns out, it’s more like yoga on a tightrope.

- Fixed-rate mortgage: Your interest rate’s locked in, like a trusty old pickup truck that just keeps chugging. No surprises, but maybe higher upfront costs.

- Adjustable-rate mortgage: Starts low, feels like a steal, but can spike like gas prices after a hurricane. Risky if you’re not ready for it.

I learned this the hard way when I almost signed an ARM with a teaser rate that’d jump after five years. My buddy, Jake, who’s annoyingly good with money, saved me by pointing out I’d be screwed if rates shot up. Check out Bankrate’s mortgage comparison guide for a clearer breakdown than my panicky notes.

My Kitchen Table Mortgage Meltdown

Picture this: me, 11 p.m., surrounded by pizza boxes and a flickering laptop screen, trying to understand mortgage rates. The air smells like burnt coffee, and I’m Googling “fixed vs adjustable mortgage” like it’s a life-or-death exam. I was so stressed I accidentally spilled coffee on my loan docs—yep, that’s the stained contract in my featured image. I kept thinking, “Will a fixed-rate mortgage save me from this chaos, or is an ARM gonna let me afford that dream house now?” Spoiler: I overthought it and ate an entire bag of chips.

Fixed-Rate Mortgages: My Safe Bet (But Boring)

A fixed-rate mortgage is like marrying your high school sweetheart—stable, predictable, but maybe not thrilling. You lock in your interest rate for the whole loan term, usually 15 or 30 years. My current place has a 30-year fixed at 6.2%, and yeah, it’s not sexy, but I sleep okay knowing my payment won’t budge. According to Freddie Mac’s rate trends, fixed rates in 2025 are hovering around 6-7%, which ain’t cheap but feels safer than an ARM’s rollercoaster.

Why I Kinda Love the Fixed-Rate Life

- No surprises: My budget’s tight, and I can’t handle payments jumping like my heart rate when I check my bank account.

- Long-term planning: I’m dreaming of turning my garage into a music studio someday. Fixed payments help me save for that.

- Peace of mind: I’m not lying awake wondering if rates will hit 10% in five years.

But here’s the catch: fixed-rate mortgages often start with higher rates than ARMs. When I signed mine, I felt like I was overpaying, like buying the expensive organic apples when the regular ones are fine. Still, I’d rather overpay now than panic later.

Adjustable-Rate Mortgages: Tempting but Sketchy

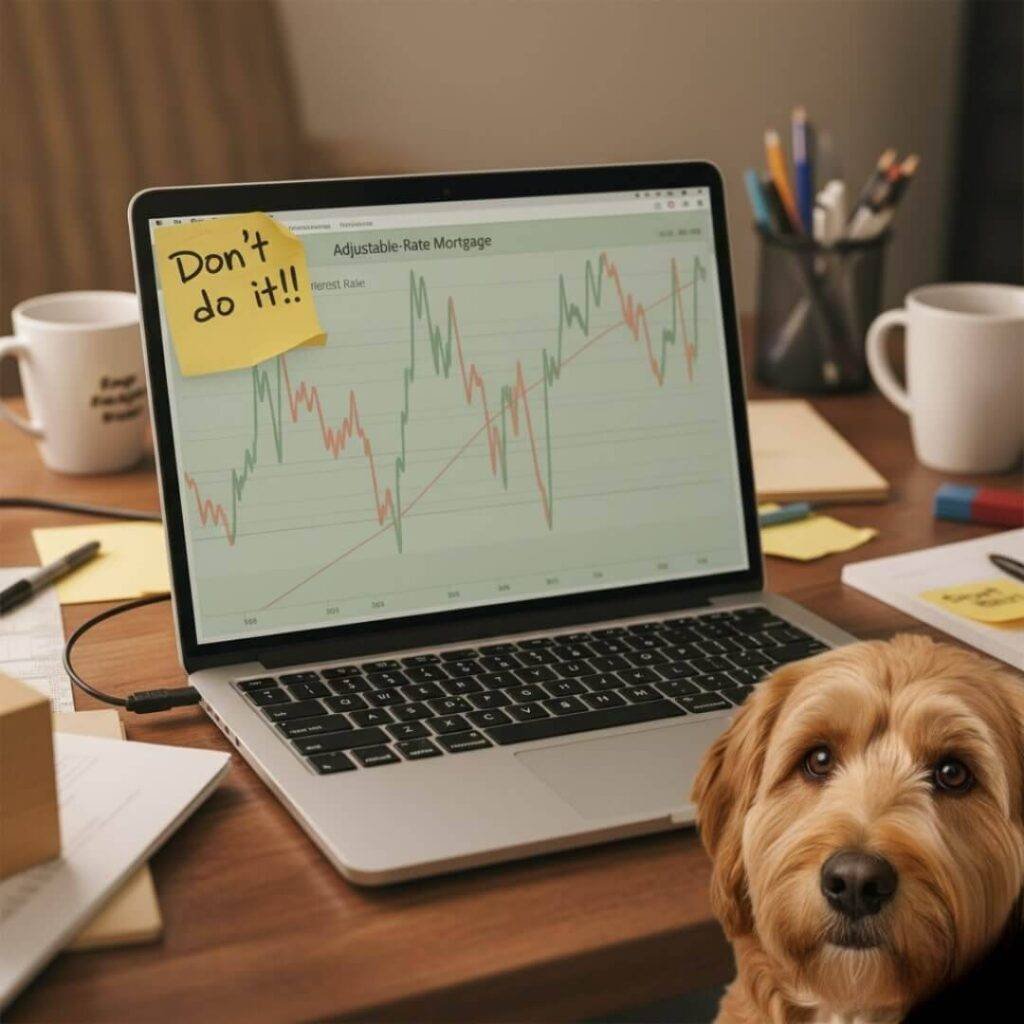

Okay, adjustable-rate mortgages? They’re like dating someone super charming who might ghost you. The rate starts low—sometimes way low, like 4.5% in 2025, per Mortgage News Daily—but it can adjust after a set period (say, 5 or 7 years). I was this close to signing a 5/1 ARM back in Columbus because the low rate meant I could afford a bigger house. But then I remembered my cousin Lisa, who got burned when her ARM adjusted and her payment shot up $400 a month. Yikes.

Why ARMs Freak Me Out (But Might Work for Some)

- Lower initial payments: Great if you’re broke now and banking on a raise later. I wasn’t.

- Risk of rate hikes: If the economy goes wild, your rate could climb faster than my dog chasing a squirrel.

- Good for short-term plans: If you’re flipping a house or moving soon, an ARM might save you cash.

I’m too much of a worrier for an ARM. I’d be checking interest rate forecasts like a weather app during a storm. But if you’re a risk-taker, maybe it’s your vibe. Just don’t say I didn’t warn you.

Which Saves More Long Term? My Messy Take

Here’s where I get real: I don’t know what’s best for everyone. Fixed vs adjustable mortgage savings depend on your life. If you’re staying put forever (like me, dreaming of that music studio), a fixed-rate mortgage probably saves you from future rate spikes. ARMs can save you upfront if you’re smart and sell before the rate adjusts. I ran some numbers on a mortgage calculator from NerdWallet, and a $300,000 fixed loan at 6.2% costs about $1,800/month for 30 years. An ARM at 4.5% starts at $1,500 but could hit $2,200 if rates jump to 8%. Long term? Fixed feels safer, but ARMs can win if you’re strategic.

My Big Mortgage Mistake

I gotta confess: I almost didn’t shop around for lenders. I was so overwhelmed I nearly went with the first bank that approved me. Dumb move. I saved like $10,000 over the loan term by comparing rates on LendingTree. Don’t be like me, sweating in my car outside the bank, thinking I had no options. Shop around, seriously.

Wrapping Up This Mortgage Mess

So, fixed vs adjustable mortgage? I’m team fixed-rate because I’m a nervous wreck who needs stability. But if you’re bolder than me (not hard), an ARM might save you some cash upfront. Either way, do your homework—unlike me, who learned the hard way with coffee stains and late-night panic. Check out those links, run the numbers, and maybe don’t eat a whole bag of chips while deciding. Got thoughts on this? Hit me up in the comments or on X—I’m curious what you’d pick!

{kind=link}